From Frank Wouters on behalf of the Dii Leadership Team

Since February 28 when the war between the US and Israel with Iran started, we have witnessed a dramatic impact on global energy markets. The price of oil is inching towards $150 per barrel, with $200 no longer a fata morgana. Meanwhile, shortages of LPG – essential for cooking – are hurting India, which has even suspended natural gas cremations to conserve fuel supply. This week, I saw a long queue of trucks waiting for diesel at a filling station in Lusaka, Zambia, and I couldn’t find diesel for my car at any of the 4 filling stations I drove to. In Europe, Korea and elsewhere, natural gas prices are spiking, while share prices of coal companies are surging. Secondary products like Helium, essential in chip manufacturing, and Sulphur, essential in copper production are also stuck in the Gulf, impacting several markets. About 20% to 30% of global seaborne fertilizer exports originate from the Gulf, and most of it must reach global markets through the Strait of Hormuz. The impact on food supply can be catastrophic for many. The list is long and expanding. Many analyses are being published, and every self-respecting consultant and thinktank has jumped on board the resilience narrative train.

Where does Dii Desert Energy stand?

Our home turf are countries with deserts, mainly in the Middle East and North Africa, but also further away such as China and Mongolia. However, we also have many partners in Europe, Japan, Korea, and other places, with an interest in the MENA region, our work and network. Countries are impacted very differently.

Egypt has been hit hard by rising oil and LNG prices and the loss of LNG from Qatar. Egypt is a net oil importer and depends on imports for about one-third of its natural gas supply. Roughly half of this comes from Israel, with LNG making up the remainder. Israeli supplies have been suspended, while Qatar accounted for a large chunk of LNG shipments that Egypt had ordered for its summer supply. As an immediate response, from March 28, malls, restaurants, and retailers will begin shutting at 9 p.m. on weekdays, a massive cultural shift for a country whose citizens like to go out late. The country also plans to turn off illuminated billboards and reduce public lighting, and government buildings will close by 6 p.m. On the positive side of the equation, Egypt’s exports of fertilizer and aluminium will command higher prices, as sales from the Gulf are blocked. And perhaps the tourism sector could benefit from the misfortunes of Dubai. But overall, the net effects will be negative for Egypt.

The impact on Morocco will also be mixed. As a net energy importer, the country will be hit hard by the increase in oil prices, but this will be offset to some extent by the surge in fertilizer prices: Morocco is one of the world’s largest exporters of phosphate fertilizers. However, production costs will be inflated by higher prices of imported ammonia.

Saudi Arabia and the UAE are managing to bypass the Strait of Hormuz via pipelines to terminals outside the Gulf. The East-West pipeline across Saudi Arabia to Yanbu on the Red Sea has the capacity to deliver 5 million barrels/day (b/d), while the pipeline from Abu Dhabi to Fujairah, on the Gulf of Oman, can carry 1.5 million b/d, although the real operational capacity for both pipelines is probably lower. Even at full capacity these routes can only cover about one-quarter of the oil that normally goes through the Strait of Hormuz. Higher oil prices may compensate some of the losses for the UAE and Saudi Arabia, but other Gulf oil and gas exporters do not share this benefit.

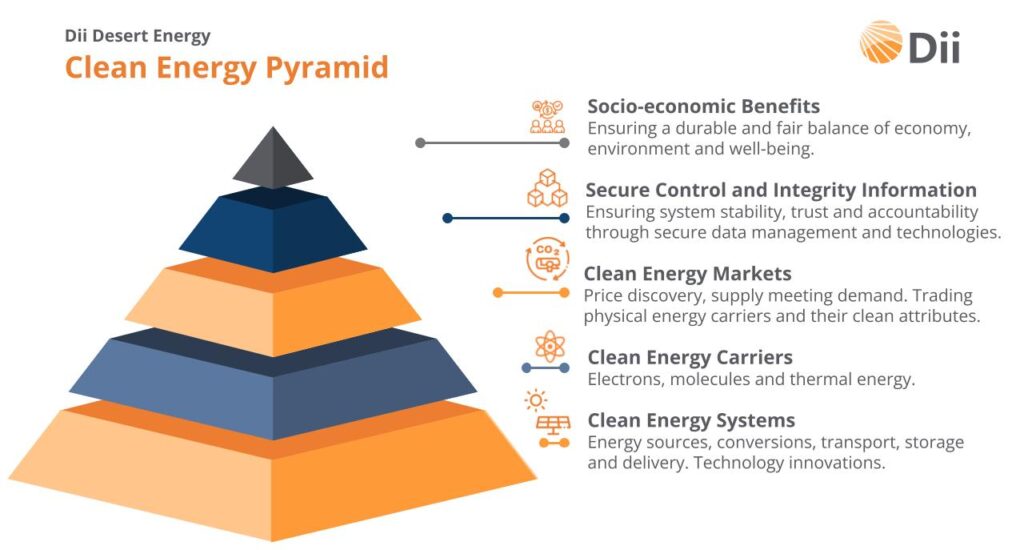

Dii’s mission is no emissions, which informs our strategy. Considering the current chaos, let us reflect on our strategic guidance. Recently we have been using the clean energy pyramid (see Figure 1) to graphically show our approach.

- The basis of the pyramid is the clean energy system, consisting of energy carriers, infrastructure for transport, storage and delivery of energy, innovation and development. This is the realm of work we have done on interconnectors, scenarios, market research, the speed of the energy transition, strategic reserves and much more. The MENA Hydrogen Alliance’ focus lies here.

- The second layer of the pyramid deals with clean energy markets, which covers price discovery, supply and demand dynamics, trading physical energy products and virtual emission-related certificates or characteristics. Our Zero Emission Traders Alliance was established to advance and promote markets and mechanisms.

- The third layer consists of secure information carriers. Technology that builds trust and enables trading and optimised control of energy assets and processes are dealt with here. The Kaspa Industrial Initiative (Kii) is currently building ecosystems tackling this prerogative.

- At the top of the pyramid sits socio-economic benefits, reflecting on a fair balance of economic interests, environmental benefits and well-being.

We believe that the current global chaos caused by the Iran war supports our mission. The shift away from fossil fuels to a more diversified clean energy system relying on renewables is more relevant than ever. Every corner of the planet has potential for renewable energy, albeit at different scales and price points. Markets will determine where and how future energy will be produced and used. Every country and region is well-advised to maximize local production of renewable energy in whatever form is best suited for the local markets. But we also know that not every country or region has the potential to be energy self-sufficient, at least not in an economic sense. Nevertheless, renewable energy at scale enables a much more diversified energy landscape, providing a more robust and resilient global energy system, if we do it well. Dii is a think tank for our industry partners providing strategic guidance in the short and long term. The following no-regret recommendations towards more resilience transpire:

- Efficiency first: Perhaps the least sexy element of the energy transition is the energy we don’t need. Insulating buildings, advanced glazing, more efficient lighting and cleaner vehicles for example are in most cases “in the money” immediately but often need a regulatory push. We can do better avoiding if not eliminating wasting energy. Demand side management is another example that is often not implemented because of regulatory hurdles. There is hardly a downside to efficiency improvement or demand side management though, and we currently see many countries implementing energy saving measures to soften the impact on their economies due to limited energy supply. We suggest making these measures permanent.

- Accelerate the build-out of domestic renewable energy capacity: This should be a no-brainer, but many countries recently slowed down renewable energy build-out, despite global growth of renewables. Whether it’s the US administration’s attacks on renewable energy, or Europe’s inability to tackle stifling regulation, we can and must do more and faster. In our peer-reviewed paper “Faster, Cheaper and Much Cleaner”, we analyzed the cost and environmental differences between an accelerated, delayed, and gradual pathway for a large, advanced economy towards zero emissions by 2050. The results were very clear: a delayed transition is 20% more expensive than the gradual transition, and a whopping $7.7 trillion more expensive than the accelerated pathway, with 4 times higher emissions of CO2. The global target of tripling renewables by 2030 is still within reach and must now become a non-negotiable target.

- Build and strengthen alliances and infrastructure: Despite the current disruption and dependency-anxiety, we believe that trade of energy will remain an important aspect of the global energy system. For trade of clean energy, new infrastructure such as pipelines, ports and interconnectors is often required. This typically requires a political framework to manage risks and channel investments. The India–Middle East–Europe Economic Corridor (IMEC) is an example. IMEC is a massive, multi-modal infrastructure project designed to connect India to Europe through the Middle East, with a strong energy component. It was officially launched at the G20 Summit in New Delhi in September 2023, but the reality is that not much has happened in the past 2.5 years. Now is the time to revive it.

- Build strategic hydrogen reserves: In 2024 we analyzed the strategic energy storage rationale for the European Union. Europe has strategic reserves for oil and gas and will in the future require strategic reserves for hydrogen and derivatives to cushion price shocks and guarantee energy security. Batteries store energy for hours, pumped hydro for days, but molecules can store energy over a season. In the short term a strategic reserve could provide additional resilience and at the same time accelerate the clean hydrogen economy by disconnecting supply from demand. In line with current practice, we propose a strategic reserve for the EU of 25% of annual demand, implying 1.7 million tonnes of hydrogen and derivatives by 2030. Other countries would be advised to consider a similar strategic reserve of clean molecules.

Of course, nobody knows what the coming days, weeks and months will bring, but the shock to the global energy system is real. Even if the hostilities end soon and the Strait of Hormuz opens again, the impact will be felt for a long time. Governments and companies are currently reassessing their strategies, supply chains and partnerships. We believe that the above recommendations will serve everyone, whatever the outcome of the current situation.